April 22, 2022

| Re: | Virax Biolabs Group Limited | |

| Registration Statement on Form F-1 | ||

| Filed March 18, 2022 | ||

| No. 333-263694 |

Ms. Abby Adams

Division of Corporation Finance

Office of Life Sciences

Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

Dear SEC Officers:

On behalf of Virax Biolabs Group Limited (the “Company”), we have set forth below responses to the comments of the staff (the “Staff”) of the Securities and Exchange Commission contained in its letter dated March 9, 2022 with respect to the Registration Statement on Form F-1, No. 333-263694 (“F-1”), submitted on March 18, 2022 by the Company. For your convenience, the text of the Staff’s comments is set forth below in bold, followed in each case by the Company’s responses. Please note that all references to page numbers in the responses are references to the page numbers in revised Form F-1 (the “Revised F-1”), filed concurrently with the submission of this letter in response to the Staff’s comments.

Registration Statement on Form F-1 filed March 18, 2022

Cover Page

1. We refer to comment 2 in our letter dated January 28, 2022. Please revise to discuss that the U.S. Senate pass the Accelerating Holding Foreign Companies Act and include a cross-reference to the more detailed disclosure in the related risk factor on page 56.

Response: In response to the Staff’s comment, the Company has revised the relevant disclosure on the cover page of the Revised F-1.

2. We note your disclosure that you do not believe you are “directly” subject to recent regulatory actions and statements by the PRC government on the regulation of business operations in China. If there is uncertainty as to the applicability of such regulatory actions, revise to explain the basis for such uncertainty.

Response: In response to the Staff’s comment, the Company has revised the relevant disclosure on the cover page of the Revised F-1. The Company respectfully submit that it is not subject to these regulatory actions or statements, as the Company does not have a variable interest entity structure and its business does not involve the collection of user data, implicate cybersecurity, or involve any other type of restricted industry.

3. We refer to comment 4 in our letter dated January 28, 2022 and reissue the comment. You state that within the organization, investor cash flows have all been received by Virax Cayman. You also state that cash to fund Virax Cayman’s operations is transferred from Virax Cayman down through your Singapore, Hong Kong, and BVI entities and then into your Chinese entities through capital contributions and loans. On the cover page, quantify any cash flows and transfers of other assets by type that have occurred to date between the holding company and its subsidiaries and direction of transfer. You also state that transfers among your Singapore, Chinese and Hong Kong entities are not restricted. However, we note the following disclosure on pages 8-9:

| ● | Further, the PRC government imposes controls on the convertibility of RMB into foreign currencies and, in certain cases, the remittance of currency out of China. |

| ● | Further, investment in Chinese companies, which are governed by the Foreign Investment Law, and the dividends and distributions from each of HKco, Virax Immune T-Cell, Shanghai Xitu are subject to relevant regulations and restrictions on dividends and payment to parties outside of China |

We note also your risk factor disclosure beginning on page 48 highlighting the risks that any funds you transfer to your PRC subsidiary are subject to approval by or registration with relevant governmental authorities in China and that PRC regulations impose restrictions on currency exchange. Please revise your disclosure on the cover page to address these limitations on your ability to transfer cash through your organization. Please make similar revisions to your discussion under the heading “Transfer of Cash Through our Organization” so that you do not assert or imply that your ability to transfer cash is unrestricted. Please also disclose if you have specific cash management policies and procedures in place that dictate how funds are transferred through your organization and if applicable, describe these policies and procedures.

Response: In response to the Staff’s comment, the Company has revised the relevant disclosures on the cover page, pages 10 and 11 of the Revised F-1.

4. We note your disclosure on page 140 that holders of Class B ordinary shares shall have the right to ten votes for each share held. Please disclose on your prospectus cover, in your summary and in your risk factors the disparate voting rights of each class of ordinary shares. In your risk factors, please discuss the risks posed by such capital structure, including but not limited to, risks relating to the potential effects on the price of your Class A ordinary shares, dilution upon conversion of the Class B ordinary shares into Class A ordinary shares and that the dual-class structure may render your shares ineligible for inclusion in certain stock market indices, which could adversely affect share price and liquidity. Additionally, if you will be considered a controlled company, please include disclosure of your controlled company status on the prospectus cover page and state whether you intend to rely on exemptions from listing standards as a controlled company.

Response: In response to the Staff’s comment, the Company has added the relevant disclosures on the cover page, pages 14, 16, 17, 62, and 63 of the Revised F-1 and added the relevant risk factors under the headings of “Our dual-class voting structure will limit your ability to influence corporate matters and could discourage others from pursuing any change of control transactions that holders of our Class A ordinary shares and Class B ordinary shares may view as beneficial,” “The dual-class structure of our ordinary shares may adversely affect the trading market for our Class A ordinary shares,” and “[We will be a “controlled company” within the meaning of the Nasdaq Stock Market Rules and, as a result, may rely on exemptions from certain corporate governance requirements that provide protection to shareholders of other companies],” in the Revised F-1.

Prospectus Summary, page 1

5. Please revise your statement that you have been operating since 2013 to clarify that prior to 2020, your operations consisted of food importation into the PRC, as referenced on page 72. Additionally, please revise your reference to your “product portfolio,” here and throughout your registration statement, to make clear that you act as distributor of products sourced from third-parties. Your disclosure should not imply that you have developed IVD test kits.

Response: In response to the Staff’s comment, the Company has revised and added the relevant disclosures on pages 1, 2, 21, 75, 97 and 102 of the Revised F-1.

6. We note your response to comment 4. Please revise the risk factor beginning “The regulatory environment for IVD could change” on page 33 to correspond to the revised disclosure regarding the challenges you face on page 4. To the extent the risk described below that heading addresses the different risk that you may not be able to demonstrate your product candidates are safe and effective, address those risks in a separate risk factor.

Response: In response to the Staff’s comment, the Company has revised and added the relevant disclosures under the risk factor headings “The regulatory environment for IVD could change, resulting a new procedure for achieving approvals for various global marketplaces which might adversely affect Virax’s ability to enter various markets” and “If we are not successful in obtaining regulatory approvals for our Virax Immune products, we may not be able to commercialize our products in the expected timeframe or at all, and our ability to expand our business and achieve our strategic objectives would be impaired,” on pages 23 and 37 of the Revised F-1.

2

7. We reissue comment 5 in part. Further revise to clarify from where you conduct what aspects of your business, including where you conduct the majority of your business, particularly in light of the revised disclosure that you have 6 employees, two of whom are engaged in research and development in addition to acting as your Chief Executive Officer and Chief Operating Officer. Clarify where your officers are located, so that investors are aware of difficulties they may have, for example, in pursuing claims or enforcing judgments. We note the varied disclosure regarding the location of your operations:

| ● | On the cover page, you state that you “conduct a substantial majority of [your] operations through [your] operating entities established in Singapore and the British Virgin Islands, primarily Virax Biolabs Pte. Limited and Logico Bioproduct Corp., which [you] we refer to as SingaporeCo. and Logico BVI, respectively. .. . . However, some of [your] operations are currently conducted through . . . operating entities established in Hong Kong and Shanghai, primarily Virax Biolabs Limited, Virax Immune T-Cell Medical Device Company Limited, and Shanghai Xitu Consulting Co., Limited.” |

| ● | On pages 1 and 69, you state that you “conduct [your] substantial operations in the United Kingdom and Hong Kong with operating subsidiaries in Singapore, China and British Virgin Islands and have been operating since 2013.” |

| ● | On page 118, you state they “conduct [your] material business operations in Singapore.” |

| ● | On page 116 you address laws in the People’s Republic of China in which you must participate due to “hav[ing] some operations located in the PRC.” |

Additionally, you state on page 5 that your Shanghai subsidiary is primarily engaged in “procurement, warehousing, product development, and staffing management.” You state on page 109 that in many cases you instruct your third-party suppliers to ship the products directly to your customers per your order instructions. Please clarify in the summary where your suppliers are located and make clear the extent to which you source third party IVD test kits and PPE from the PRC and/or Hong Kong.

Finally, as requested in comment 5, when making statements regarding “the company,” please revise to clarify whether you refer to the holding company, or identify the subsidiary or third-party contractor to which you refer, as applicable, more specifically than the revisions to “we,” “us,” “our” or similar terms that fail to identify the relevant entity. Ensure that your disclosure throughout the filing clearly identifies the subsidiary whose operations you are referencing.

Response: In response to the Staff’s comment, the Company has revised the relevant disclosures for consistency and added the relevant disclosures on the cover page, pages ii, 1, 2, 64, 75, 76, 98, 116, 123, 125, and 179 of the Revised F-1. The Company respectfully submits that the “Company” or “Virax Cayman” is defined as Virax Biolabs Group Limited under the “Conventions that Apply to this Prospectus” section and revised the relevant disclosures where appropriate throughout the F-1.

8. We note the revised disclosure on page 8 in response to comment 7. As previously requested, further revise the disclosure in this section to disclose the approvals you are required to obtain. Also revise this section for consistency. For example, as you state that you have received all required permissions, revise the first sentence to provide a more definitive statement about the degree of government regulation to which you are subject. Further, you first state that you have obtained all approvals for Shanghai Xitu, but later refer to multiple PRC subsidiaries. Revise to clarify whether you have obtained the required approvals for all of your operations in China. We note your statement that you are not required to obtain additional permission or approval from Chinese authorities, including the CSRC and the CAC, to either approve your PRC subsidiaries’ operations or to offer the securities being registered to foreign investors. Please revise to explain how you determined that such permissions are not required. If you relied on the advice of counsel, please revise to name counsel and file such counsel’s consent as an exhibit to the registration statement.

Response: In response to the Staff’s comment, the Company has revised the relevant disclosures for consistency and added the relevant disclosures on pages 7 to 10, 15, 46 to 51, and 53 of the Revised F-1. The Company respectfully submit that only Shanghai Xitu is its only PRC subsidiary in the current corporate structure.

3

9. Revise to disclose in the summary the amount of proceeds that will be held in escrow for the benefit of the underwriters and the period of time such funds will be restricted, as referenced on page 62.

Response: In response to the Staff’s comment, the Company has added the relevant disclosures on page 18 of the Revised F-1.

Risk Factors

Risks Related to Doing Business in China and Hong Kong, page 43

10. We note numerous disclosures that reference dates that have already passed. Please update your disclosures throughout your filing. As examples only, we note the following:

| ● | On December 28, 2021, the Measures for Cybersecurity Review (2021 version) was promulgated and will become effective on February 15, 2022. |

| ● | On December 24, 2021, the CSRC released the Administrative Provisions of the State Council Regarding the Overseas Issuance and Listing of Securities by Domestic Enterprises (Draft for Comments) and the Measures for the Overseas Issuance of Securities and Listing Record-Filings by Domestic Enterprises (Draft for Comments), both of which have a comment period that expires on January 23, 2022. |

Response: In response to the Staff’s comment, the Company has revised the relevant disclosures on pages 7 to 10, 15, 46 to 52, of the Revised F-1.

Use of Proceeds , page 62

11. We reissue comment 9 in part. In the Use of Proceeds you address two strategic asset acquisitions as “potential acquisition targets.” The disclosure on page 95 states that you have entered into a non-binding letter of intent with a potential acquisition target and have identified three potential acquisition targets. First, revise these disclosures to clarify the number of targets you have identified. Second, please revise these and similar disclosure items throughout your document to clarify if you are addressing the purchase of intellectual property as opposed to an entire company.

Additionally, you state on page 31 that your Virax Immune brand’s future success depends, in part, of your ability to acquire the necessary proprietary technology from a European Union based materials technology company. Please revise to make clear in the summary the extent to which the development of your T-Cell IDV test is dependent upon this acquisition.

Response: In response to the Staff’s comment, the Company has revised the relevant disclosures on pages 3, 13, 35, and 99, 100, and 102 of the Revised F-1. The Company respectfully submit that it has highlighted the “Failure to partially acquire the proprietary technology from a European Union based materials technology company could have an adverse effect on our planned results of operations for our Virax Immune brand and our business”

Management Discussion and Analysis of Financial Condition and Results of Operations Overview, page 69

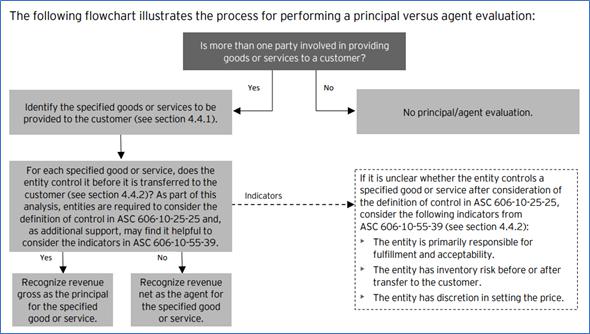

12. We note the revised discussion provided in response to comment 10 on page 70. We also note the revisions on page 1 whereby you state that you act as distributors of third-party suppliers’ products. Provide us your analysis of the considerations in ASC 606-10- 55-36 through 55-40 in determining how to reflect distributor revenue in your financial statements.

Response: In response to the Staff’s comment, the Company’s analysis of the considerations in ASC 606-10- 55-36 through 55-40 in determining how to reflect distributor revenue in its financial statements is as follows:

In the Company’s analysis of ASC 606-10-55-36 through 55-40, Principal versus Agent Considerations, its analysis covered each distinct product in the ViraxClear and ViraxCare product lines. Regarding the distinction, the Company followed the guidelines under ASC 606-10-25-19 through 25-22 and it was determined that each product will be treated the same under the Principal versus Agent consideration in ASC 606-10- 55-36 through 55-40.

For the nature of ASC 606-10- 55-36 through 55-40, the Company identified the product to be provided to the customer and assessed whether it controlled that product before the product is then transferred to the customer.

4

In its assessment, in conjunction with the ASC codification language, the Company also used the following flowchart produced by Ernst & Young:

In the Company’s assessment, it is determined that it obtained control of the product in addition to obtaining legal title that it is distributing to its customers as the Company physically takes control, obtains legal title and stores the product in the warehouse.

Its evaluation that one of its operating subsidiary controls the product before transferring it to the customer are as follows:

| 1. | The entity is responsible for fulfilling the promise to provide the specified good or service. |

| ● | The relevant operating subsidiary is responsible for the brand and the sale to the customer. The company manages the brand image and presentation of our products to the customer, which includes the responsibility customer acceptability. |

| 2. | The entity has inventory risk before the specified good or service has been transferred to a customer or after transfer of control to the customer. |

| ● | The relevant operating subsidiary owns the inventory and has inventory risk until it is shipped to the customer from the warehouse. The relevant operating subsidiary is also obligated to take back any product returns from the customer and is at risk for any unsold products. |

| 3. | The entity has sole discretion in establishing the price for the specified good or service. |

| ● | The relevant operating subsidiary establishes the price for the products that are sold to the customer. |

Based on the aforesaid, the Company’s assessment is that the relevant operating subsidiary acts as the Principal and not an agent and recognizes revenue in the gross amount of consideration in exchange for each product.

Business

Key Customer Relationships, page 111

13. We note your disclosure that five customers and three customers accounted for approximately 98% and 100% of your sales for the years ended March 31, 2021 and 2020, respectively. Please add risk factor disclosure highlighting the risks related to customer concentration.

Response: In response to the Staff’s comment, the Company has added the relevant risk factor under the heading “We have a significant customer concentration, with a limited number of customers accounting for a large portion or all of our revenues” on pages 13 and 26 of the Revised F-1.

Research and Development, page 112

14. We note your revised disclosure in response to comments 12 and 16. Revise your disclosure here and wherever you address your “research and development team” to clarify, if true, that your research and development team consists of your Chief Executive Officer and Chief Operating Officer, who fulfil those roles in addition to their duties as CEO and COO, respectively.

Response: In response to the Staff’s comment, the Company has added the relevant disclosures on pages 4, 100, 119 and 122 of the Revised F-1.

5

Employees and Human Capital , page 116

15. Please revise to remove from this section your discussion of “externally employed” employees. We will not object to a cross reference to your third-party contractual arrangements described elsewhere in the prospectus.

Response: In response to the Staff’s comment, the Company has removed the relevant disclosures on page 122 of the Revised F-1.

Regulations, page 118

16. Please add a section here discussing PRC laws and regulation applicable to your business.

Response: In response to the Staff’s comment, the Company has added the relevant sub-section discussing PRC laws and regulation applicable to Shanghai Xitu starting on pages 131 and 132 of the Revised F-1.

Enforcement of Civil Liabilities , page 168

17. We note your disclosure that most of your directors and executive officers are nationals or residents of jurisdictions other than the United States and substantially all of their assets are located outside the United States. Please revise your disclosure here and in the related risk factor on page 48 to affirmatively state whether any of your officers, directors or other members of senior management are located in China or Hong Kong. If so, disclose that their residence in China may make it even more difficult to enforce any judgments obtained from foreign courts against such persons compared to other non-U.S. jurisdictions.

Response: In response to the Staff’s comment, the Company has revised the relevant disclosures on pages 2, 64, 179 of the Revised F-1.

Exhibits

18. Please revise Exhibit 5.1 to provide an opinion on the legality of the Ordinary Shares. Paragraph three provides the opinion on the Underwriter’s Warrants and the Ordinary Shares underlying the Underwriter’s Warrants, but not the Ordinary Shares.

Response: The Company respectfully submits that Exhibit 5.1, Opinion of Ogier, provides an opinion on the legality of the Ordinary Shares, while Exhibit 5.2, Opinion of Loeb & Loeb LLP, provides the opinion on the Underwriter’s Warrants and the Ordinary Shares underlying the Underwriter’s Warrants.

19. With respect to exhibits 5.1, 5.2, 10.5, and 10.6, replace the “Form of” legal opinions and employment agreements with the finalized agreements. Refer to Item 601(b)(5) and (b)(10)(iii) of Regulation S-K..

Response: In response to the Staff’s comment, the Company has filed the finalized agreements for Exhibits 10.5 and 10.6 under Exhibits 10.7 to 10.14 of the Revised F-1. The Company respectfully submits that the finalized exhibits 5.1 and 5.2 will be filed by amendment.

20. Clarify the authority upon which Messrs. Nortan and Erez and Ms. Gilmour signed the registration statement as directors. We note from the footnote to the Directors and Executive Officer’s table on page 124 that their appointment as directors will not be effective until the registration statement is declared effective.

Response: In response to the Staff’s comment, the Company has amended the relevant disclosures on page II-7 of the Revised F-1.

6

Should you have any questions relating to the foregoing or wish to discuss any aspect of the Company’s filing, please contact me at +852.5600.0188.

| Very truly yours, | |

| /s/ Lawrence S. Venick | |

| Lawrence S. Venick |

7