As filed with the Securities and Exchange Commission on June 24, 2022.

Registration Statement No. 333-263694

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________

Form F-1

(Amendment No. 6)

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

_______________

Virax Biolabs Group Limited

(Exact name of Registrant as specified in its charter)

_______________

Not Applicable

(Translation of Registrant’s name into English)

_______________

|

Cayman Islands |

2835 |

Not Applicable |

||

|

(State or other jurisdiction of |

(Primary Standard Industrial |

(I.R.S. Employer |

30 Broadwick Street

London, W1F 8LX

United Kingdom

Telephone: +44 020 7788 7414

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

_______________

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

+1 800-221-0102

(Name, address, including zip code, and telephone number, including area code, of agent for service)

_______________

Copies of all communications, including communications sent to agent for service, should be sent to:

|

Lawrence S. Venick, Esq. |

Richard I. Anslow, Esq. |

_______________

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act: Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), may determine.

____________

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

EXPLANATORY NOTE

This Registration Statement contains two prospectuses, as set forth below.

• Public Offering Prospectus. A prospectus to be used for the public offering of 1,350,000 Ordinary Shares of the Registrant (the “Public Offering Prospectus”) through the underwriter named on the cover page of the Public Offering Prospectus.

• Resale Prospectus. A prospectus to be used for the resale by the selling shareholders set forth therein of 1,944,784 Ordinary Shares of the Registrant (the “Resale Prospectus”).

The Resale Prospectus is substantively identical to the Public Offering Prospectus, except for the following principal points:

• they contain different outside and inside front covers and back covers;

• they contain different Offering sections in the Prospectus Summary section beginning on page 1;

• they contain different Use of Proceeds sections on page 67;

• a selling shareholder section is included in the Resale Prospectus;

• a selling shareholder Plan of Distribution is inserted; and

• the Legal Matters section in the Resale Prospectus on page 172 deletes the reference to counsel for the underwriter.

The Registrant has included in this Registration Statement a set of alternate pages after the back cover page of the Public Offering Prospectus (the “Alternate Pages”) to reflect the foregoing differences in the Resale Prospectus as compared to the Public Offering Prospectus. The Public Offering Prospectus will exclude the Alternate Pages and will be used for the public offering by the Registrant. The Resale Prospectus will be substantively identical to the Public Offering Prospectus except for the addition or substitution of the Alternate Pages and will be used for the resale offering by the selling shareholders.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

|

PRELIMINARY PROSPECTUS (SUBJECT TO COMPLETION) |

DATED JUNE 24, 2022 |

1,350,000 Ordinary Shares

Virax Biolabs Group Limited

This is the initial public offering of our ordinary shares (“Ordinary Shares”). We are offering 1,350,000 of our Ordinary Shares, par value $0.0001 per share, on a firm commitment basis. The estimated initial public offering price is expected to be $5.00 per share. The selling shareholders (as defined herein) is offering 1,944,784 Ordinary Shares to be sold in the offering pursuant to the Resale Prospectus. We will not receive any proceeds from the sale of the Ordinary Shares to be sold by the selling shareholders. Currently, no public market exists for our Ordinary Shares. We have applied to list our Ordinary Shares listed on the Nasdaq Capital Market, or Nasdaq, under the symbol “VRAX”. We cannot guarantee that we will be successful in listing our Ordinary Shares on the Nasdaq; however, we will not complete this offering unless we are so listed.

We are both an “emerging growth company” and a “foreign private issuer” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings. See “Prospectus Summary — Implications of Being an Emerging Growth Company and a Foreign Private Issuer” for additional information. Investors are cautioned that you are buying shares of a shell company issuer incorporated in the Cayman Islands with operating subsidiaries in Singapore, China, Hong Kong and British Virgin Islands, investors will not hold direct equity investments in our China and Hong Kong operating subsidiaries. Our ordinary shares offered in this prospectus are shares of our Cayman Islands holding company.

We will not be a “controlled company” under the NASDAQ Stock Market Rules post public offering.

Investing in our Ordinary Shares is highly speculative and involves a significant degree of risk. Virax Biolabs Group Limited, which we refer to as Virax Cayman, is a holding company incorporated in Cayman Islands. As a holding company with no material operations of our own, Virax Cayman conduct a substantial majority of our sales and trading activities through our operating entity established in Singapore, Virax Biolabs Pte. Limited, which we refer to as SingaporeCo. Currently, Virax Cayman indirectly owns 95.65% of the equity interests in SingaporeCo. However, some of Virax Cayman’s operations are currently conducted through our operating entities established in the British Virgin Islands, Hong Kong and Shanghai, primarily, Logico Bioproducts Corp., Virax Immune T-Cell Medical Device Company Limited and Shanghai Xitu Consulting Co., Limited, which we refer to as Logico BVI, Virax Immune T-Cell and Shanghai Xitu, respectively. Our ordinary shares offered in this prospectus are shares of our Cayman Islands holding company.

Recent statements by the Chinese government have indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investments in China based issuers. Any future action by the Chinese government expanding the categories of industries and companies whose foreign securities offerings are subject to government review could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and could cause the value of such securities to significantly decline or be worthless.

Recently, the PRC government initiated a series of regulatory actions and made a number of public statements on the regulation of business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using a variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding efforts in anti-monopoly enforcement. We are not subject to these regulatory actions or statements, as we do not have a variable interest entity structure and our business does not involve the collection of user data, implicate cybersecurity, or involve any other type of restricted industry. Because these statements and regulatory actions are new, however, it is highly uncertain how soon legislative or administrative regulation making bodies in China will respond to them, or what existing or new laws or regulations will be modified or promulgated, if any, or the potential impact such modified or new laws and regulations will have on our daily business operations or our ability to accept foreign investments and list on an U.S. exchange.

The Holding Foreign Companies Accountable Act, or the HFCA Act, was enacted on December 18, 2020. In accordance with the HFCA Act, trading in securities of any registrant on a national securities exchange or in the over-the-counter trading market in the United States may be prohibited if the Public Company Accounting Oversight Board (the “PCAOB”) determines that it cannot inspect or fully investigate the registrant’s auditor for three consecutive years beginning in 2021, and, as a result, an exchange may determine to delist the securities of such registrant. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if enacted, would amend the HFCA Act and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three, thus reducing the time period before our securities may be prohibited from trading or delisted if our auditor is unable to meet the PCAOB inspection requirement. Pursuant to the HFCA Act, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in: (1) mainland China of the People’s Republic of China because of a position taken by one or more authorities in mainland China; and (2) Hong Kong, a Special Administrative Region and dependency of the PRC, because of a position taken by one or more authorities in Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. Our registered public accounting firm, BF Borgers CPA PC, is not headquartered in mainland China or Hong Kong and was not identified in this report as a firm subject to the PCAOB’s determination. Notwithstanding the foregoing, if the PCAOB is not able to fully conduct inspections of our auditor’s work papers in China, you may be deprived of the benefits of such inspection which could result in limitation or restriction to our access to the U.S. capital markets and trading of our securities may be prohibited under the HFCA Act. See “Risk Factor — Our Ordinary Shares may be prohibited from being traded on a national exchange under the Holding Foreign Companies Accountable Act if the PCAOB is unable to inspect our auditors for three consecutive years beginning in 2021. The delisting of our Ordinary Shares, or the threat of their being delisted, may materially and adversely affect the value of your investment. Our registered public accounting firm, BF Borgers CPA PC, is not headquartered in mainland China or Hong Kong and was not identified in the PACOB’s Determination Report on December 16, 2021 as a firm subject to the PCAOB’s determination.”

Within the organization, investor cash inflows have all been received by Virax Cayman. Cash to fund Virax Cayman’s operations is transferred from Virax Cayman down through our Singapore, Hong Kong, BVI entities and then into our Chinese entity through capital contributions and loans. However, the PRC government imposes controls on the convertibility of RMB into foreign currencies and, in certain cases, the remittance of currency out of China, and investment in Chinese companies, which are governed by the Foreign Investment Law and Company Law, and the dividends and distributions from Shanghai Xitu is subject to relevant regulations and restrictions on dividends and payment to parties outside of China. See “Risk Factors — Risks Related to Doing Business in China and Hong Kong — PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay us from using part of the proceeds of this offering to make loans or additional capital contributions to our PRC subsidiary, which could materially and adversely affect our liquidity and our ability to fund and expand our business” and “Restrictions on currency exchange may limit our ability to utilize our revenues effectively” for more information on the risk of PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion with respect to part of the proceeds of this offering to make loans or additional capital contributions to our PRC subsidiary and restrictions on currency exchange may limit our ability to utilize our revenues effectively with respect to our operations. Transfers among our Singapore and Hong Kong entities are not restricted under Singapore and Hong Kong Laws. No dividends or distribution have been made by our subsidiaries or by Virax Cayman to date and we intend to reinvest all cash into our subsidiaries for the foreseeable future. For the years ended March 31, 2021 and 2020 and for the six months ended September 30, 2021, there was no transfer between Virax Cayman and its subsidiaries.

Before buying any shares, you should carefully read the discussion of material risks of investing in our Ordinary Shares in “Risk Factors” beginning on page 21 of this prospectus.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

|

PER SHARE |

TOTAL |

|||||

|

Initial public offering price |

$ |

5.00 |

$ |

6,750,000 |

||

|

Underwriting discounts and commissions(1)(2) |

$ |

0.35 |

$ |

472,500 |

||

|

Proceeds, before expenses, to us |

$ |

4.65 |

$ |

6,277,500 |

||

____________

(1)The underwriter, Boustead Securities, LLC, will receive compensation in addition to the discounts and commissions. We have agreed to issue Underwriter Warrants to the underwriter as a portion of the underwriting compensation payable to the underwriter in connection with this offering. For a description of compensation payable to the underwriter, see “Underwriting” beginning on page 168.

(2) Does not include a non-accountable expense allowance equal to 0.75% of the gross proceeds of this offering, payable to the underwriter, or the reimbursement of certain expenses of the underwriter. For a description of other terms of compensation to be received by the underwriter, see “Underwriting” beginning on page 168.

We expect our total cash expenses for this offering (including cash expenses payable to our underwriters for their out-of-pocket expenses) to be approximately $171,275, exclusive of the above discounts and commissions. In addition, we will pay additional items of value in connection with this offering that are viewed by the Financial Industry Regulatory Authority, or FINRA, as underwriting compensation. These payments will further reduce proceeds available to us before expenses. See “Underwriting.”

This offering is being conducted on a firm commitment basis. The underwriters are obligated to take and pay for all of the shares if any such shares are taken. We have granted the underwriters an option for a period of forty-five (45) days after the closing of this offering to purchase up to 15% of the total number of our Ordinary Shares to be offered by us pursuant to this offering (excluding shares subject to this option), solely for the purpose of covering over-allotments, at the initial public offering price less the underwriting discounts and commissions. If the Underwriter exercises the option in full, the total underwriting discounts and commissions payable will be $621,000 based on an assumed initial public offering price of $5.00 per Ordinary Shares, and the total proceeds to us, before expenses, will be $7,141,500. If we complete this offering, net proceeds will be delivered to us on the closing date.

The underwriters expect to deliver the Ordinary Shares against payment as set forth under “Underwriting”, on or about , 2022.

BOUSTEAD SECURITIES, LLC

The date of this prospectus is , 2022.

|

Page |

||

|

1 |

||

|

21 |

||

|

65 |

||

|

66 |

||

|

67 |

||

|

68 |

||

|

69 |

||

|

70 |

||

|

71 |

||

|

73 |

||

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

74 |

|

|

89 |

||

|

96 |

||

|

124 |

||

|

132 |

||

|

145 |

||

|

146 |

||

|

147 |

||

|

160 |

||

|

162 |

||

|

168 |

||

|

171 |

||

|

172 |

||

|

172 |

||

|

173 |

||

|

176 |

||

|

F-1 |

We are responsible for the information contained in this prospectus and any free writing prospectus we prepare or authorize. We have not, and the underwriters have not, authorized anyone to provide you with different information, and we and the underwriters take no responsibility for any other information others may give you. We are not, and the underwriters are not, making an offer to sell our Ordinary Shares in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or the sale of any Ordinary Shares.

For investors outside the United States: Neither we, the selling shareholders, nor the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction, other than the United States, where action for that purpose is required. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the Ordinary Shares and the distribution of this prospectus outside the United States.

We are incorporated under the laws of the Cayman Islands and a majority of our outstanding securities are owned by non-U.S. residents. Under the rules of the U.S. Securities and Exchange Commission, or the SEC, we currently qualify for treatment as a “foreign private issuer.” As a foreign private issuer, we will not be required to file periodic reports and financial statements with the Securities and Exchange Commission, or the SEC, as frequently or as promptly as domestic registrants whose securities are registered under the Securities Exchange Act of 1934, as amended, or the Exchange Act.

Until and including , 2022 (twenty-five (25) days after the date of this prospectus), all dealers that buy, sell or trade our Ordinary Shares, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

i

CONVENTIONS THAT APPLY TO THIS PROSPECTUS

Unless we explicitly state otherwise or the context otherwise indicates clearly, all references in this proxy statement to “we,” “us,” “our,” or “our Group” refer to Virax Biolabs Group Limited and its subsidiaries, namely, Virax Biolabs (UK) Limited, Virax Biolabs Limited, Virax Immune T-Cell Medical Device Company Limited, Virax Biolabs Pte. Limited, Logico Bioproducts Corp., and Shanghai Xitu Consulting Co., Limited.

The “Company” or “Virax Cayman” refers to Virax Biolabs Group Limited.

“GBP” or “GB£” refers to the legal currency of the United Kingdom.

“HKD” or “HK$” refers to the legal currency of Hong Kong.

“RMB” or “Renminbi” refers to the legal currency of China.

“IVD” refers to in-vitro diagnostics.

“PRC” or “China” refers to the People’s Republic of China, including Hong Kong and Macau.

“Prospectus” refers to the public offering prospectus unless we explicitly state otherwise or the context otherwise indicates clearly.

“SGD” or “S$” refers to the legal currency of Singapore.

“United Kingdom” or “UK” refers to the England, Scotland, Wales and Northern Ireland for the purpose of this prospectus.

“$” or “U.S. dollars” or “USD” refers to the legal currency of the United States.

We have made rounding adjustments to some of the figures included in this prospectus. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

Unless the context indicates otherwise, all information in this prospectus assumes no exercise by the underwriters of their over-allotment option and no exercise of the Underwriter Warrants.

Our business is primarily conducted in Europe, and the financial records of our subsidiaries in Asia are maintained in USD, and our functional currency is USD. Our consolidated financial statements are presented in U.S. dollars. We use U.S. dollars as the reporting currency in our consolidated financial statements and in this prospectus.

ii

PUBLIC OFFERING PROSPECTUS SUMMARY

The following summary highlights information contained elsewhere in this prospectus and does not contain all of the information you should consider before investing in our Ordinary Shares. You should read the entire prospectus carefully, including “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our consolidated financial statements and the related notes thereto, in each case included in this prospectus. You should carefully consider, among other things, the matters discussed in the section of this prospectus titled “Business” before making an investment decision. This prospectus contains information from an industry report commissioned by us and prepared by Netscribes, an independent research firm, to provide information regarding our industry. We refer to this report as the Netscribes Report.

Overview

Virax Cayman is a holding company incorporated as an exempted company under the laws of the Cayman Islands. As a holding company with no material operations of our own, Virax Cayman conducts our operations through its operating subsidiaries in Singapore, Hong Kong, China and British Virgin Islands and has been operating since 2013. Prior to the introduction of Virax branded products in 2020, the Group was engaged in the fast moving consumer goods (“FMCG”) importation business into the PRC.

Virax Cayman is a global innovative biotechnology group that primarily engages in sales, distribution and marketing of diagnostics test kits and med-tech and Personal Protective Equipment (“PPE”) products for the prevention, detection, diagnosis and risk management of viral diseases with a particular interest in the field of immunology. Our mission is to minimize the risks of viruses throughout the world via our products offerings.

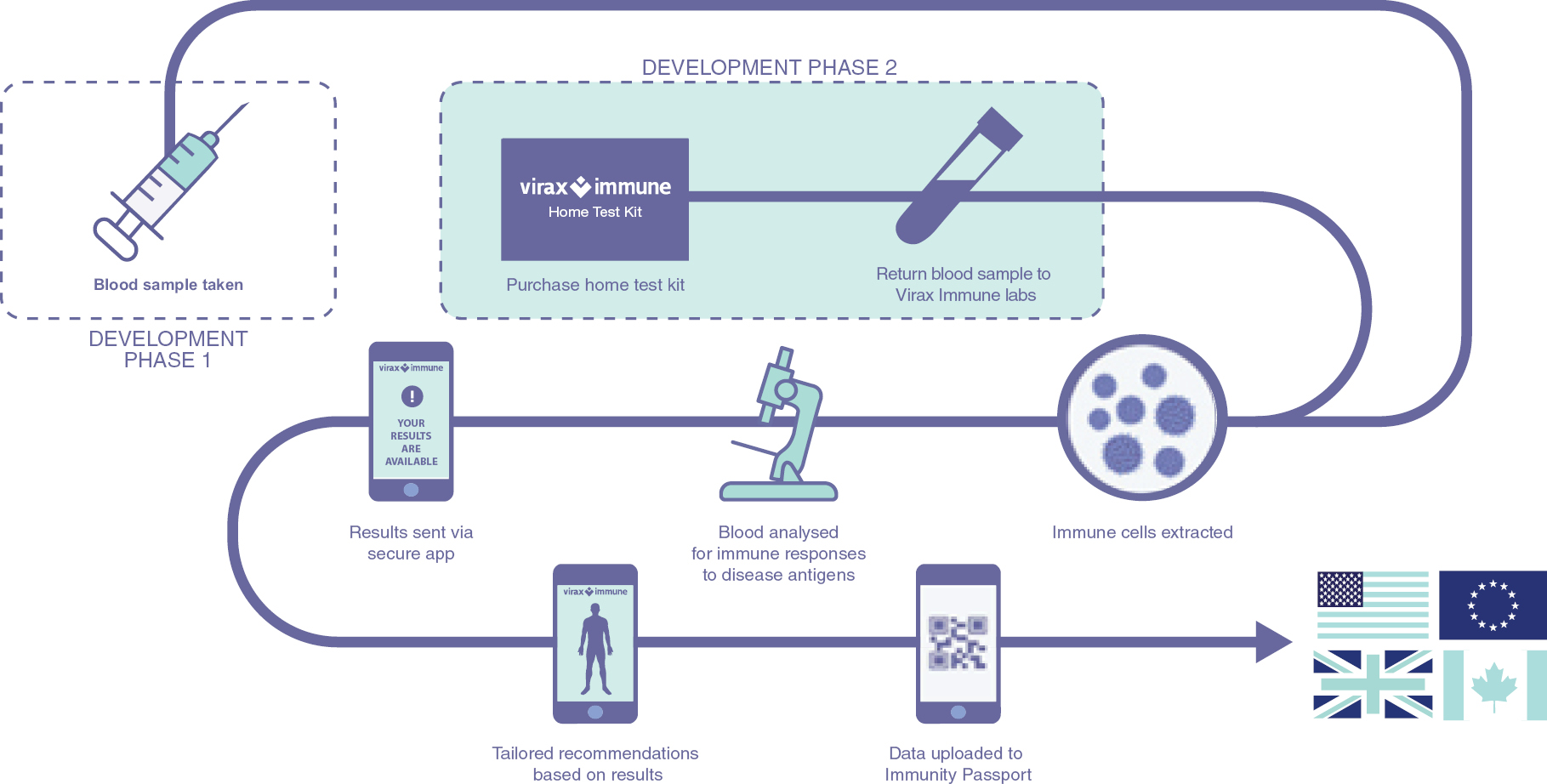

Our product portfolio includes: (i) diagnostics test kits sold through our “ViraxClear” brand; (ii) med-tech and PPE products sold through our “ViraxCare” brand; and (iii) sourced brands of third party suppliers, independent of our own brands (“Sourced Brands”). Currently, our Group does not manufacture or develop any product that we sell in our product portfolio and we act as a distributor of third-party suppliers’ products. We expect to develop and launch an upcoming brand “Virax Immune”, with the intention of providing an immunology profiling platform that assesses each individual’s immune risk profile against major global viral diseases. We believe that the T-Cell in-vitro diagnostic (“IVD”) Tests and immunology platform we are developing under the Virax Immune brand will be particularly useful in the diagnosis and threat analysis of the major viruses faced globally. As of the date of the prospectus, we have developed a functioning prototype of our T-Cell IVD Test under the Virax Immune brand but we are still in the process of conducting further tests and we have not submitted any T-Cell IVD Test to any regulatory agency for approval. Currently, our clinical trials and research activities for our T-Cell IVD Test under the Virax Immune brand are conducted by independent third party science companies, namely ICON Clinical Research Limited and IQ Services B.V., respectively, in the Netherlands. Prior to the sale of our T-Cell IVD Test under the Virax Immune brand in our targeted jurisdictions, namely, Canada, United Kingdom, the European Union and the United States, we must apply with the relevant authority for the regulatory approvals. In Canada, our T-Cell IVD Test will fall under Class I devices, which we will apply for the Health Canada Medical Device Establishment License. In the European Union, we intend to apply our T-Cell IVD Test under the self-certified Class A risk-based class route. Class A IVDs include specimen receptacles, laboratory instruments, and buffer solutions. Under the self-certified Class A risk-based class route, we do not require the involvement of a notified body to obtain the CE Marking to our T-Cell IVD Test. In the United Kingdom, as part of the transition due to the United Kingdom withdrawal from the European Union, we intend to use the recognized CE marks that we will apply with the European Union for our T-Cell IVD Test until June 30, 2023 (the “Transitional Arrangement”), after which, we will to conform with the UK IVD regime rather than relying on Transitional Arrangement and apply with the UK Medicine and Healthcare Products Regulatory Agency for a UK Conformity Assessed mark before we can sell our T-Cell IVD Test in the UK post June 30, 2023. In the United States, we intend to apply our T-Cell IVD Test under the Virax Immune brand under Class III devices (highest risk), which are subject to most of the requirements under Class I and Class II devices as well as to pre-market approval before they can be sold in the United States. For more detailed information on the Regulatory Approval on Medical Device Products with respect to our T-Cell IVD test under our Virax Immune brand, refer to “Regulations — Summary of Regulatory Approval on Medical Device Products (Relevant Jurisdictions).”

1

Currently, our Group does not develop or manufacture any product that we sell under the ViraxCare brand, the ViraxClear brand and Sourced Brands as we act as a distributor of third-party suppliers’ products. To facilitate the sales and distribution of our ViraxClear and ViraxCare products, we predominately rely on our key third-party suppliers, Nanjing Vazyme Medical Technology Co., Ltd in China for diagnostics test kits and Venus Health Consulting Limited in Hong Kong for med-tech and PPE products, for product manufacturing. After we receive our ViraxCare and ViraxClear products from our suppliers, we utilize a third party logistic company, namely, Stork Up Limited in Hong Kong, for the distribution of our products to our end-users and strategic partners overseas. However, we believe our products, in particular diagnostic test kits, provide significant value for consumers, through improved detection of diseases, improvements in health, wellness and productivity as well as by reducing other healthcare costs, such as emergency visits and hospitalizations. Our Group also seeks to maximize consumers’ access to our products and services through competitive pricing and regular evaluations of our pricing arrangements and contracts with our distributors.

Currently, the end-users of our distribution partners under our ViraxClear brand include but not limited to, clinics, pharmacies, laboratories, hospitals, and other relevant groups on an international basis, covering more than 10 countries and 4 regions, including but not limited to Europe, South America, Asia Pacific, and Sub-Saharan Africa, and Our Group expects to extend our geographical reach to North America in 2022, while the end-users of our dedicated online platforms sales under our ViraxClear brand are predominately individuals and pharmacies. The end-users of our ViraxCare products are predominately corporations, employees, and individual consumers.

Currently, as stated above, clinical trials and research activities for our T-Cell IVD Test under the upcoming Virax Immune brand are conducted by independent third party science companies in the Netherlands together with our Hong Kong subsidiary, Virax Immune T-Cell. As our Group does not manufacture or develop any product that we sell under the ViraxCare brand, the ViraxClear brand and Sourced Brands because we act as a distributor of third-party suppliers’ products, the trading and sales of these products are primarily conducted through our SingaporeCo with some trading and sales of these products through our Logico BVI which are located in Singapore and British Virgin Islands, respectively. Shanghai Xitu is located in the PRC and is primarily engaged in procurement. Further, the majority of our executive officers and directors are located outside of the United States and are nationals or residents of jurisdictions other than the United States, and all or a substantial portion of their assets are located outside of the United States. Mr. James Foster, our Chief Executive Officer, chairman of the board of directors, holds a British Passport and currently resides in Shanghai, China; Mr. Jason Davis, our Chief Financial Officer, is located in the United States and holds a United States passport; Mr. Mark Ternouth, our Chief Technical Officer, holds a British Passport and currently resides in Shanghai, China; Mr. Tomasz George, our Chief Scientific Officer, holds a British passport and currently resides in the United Kingdom; Mr. Cameron Shaw, our Chief Operating Officer and director, holds a British passport and currently resides in the United Kingdom; Mr. Yair Erez, our independent director, holds a British passport and currently resides in the United Kingdom; Mr. Evan Norton, our independent director, holds a United States passport and currently resides in the United States; and Ms. Margaret Gilmour, our independent director, holds a Canada passport and currently resides in Canada. See “Risk Factors — Because we are incorporated under the laws of the Cayman Islands, our executive office is located in the United Kingdom and all of our executive officers and directors are located outside the United States, you may face difficulties in protecting your interests, and your ability to protect your rights through the U.S. Federal or state courts may be limited” for further details on investors’ difficulties in protecting their interests, and their ability to protect their rights, including but not limited to, pursuing claims or enforcing judgments, through the U.S. Federal or state courts may be limited.

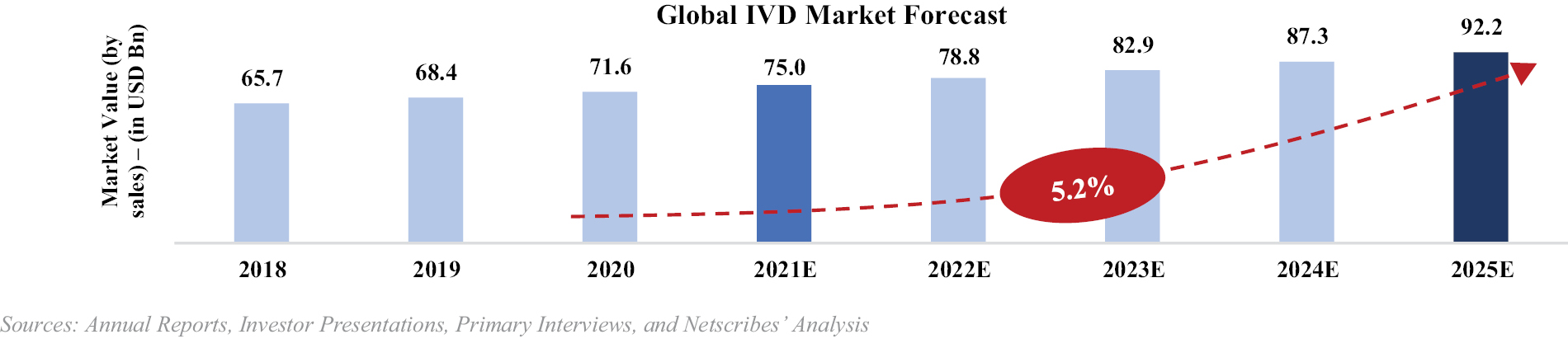

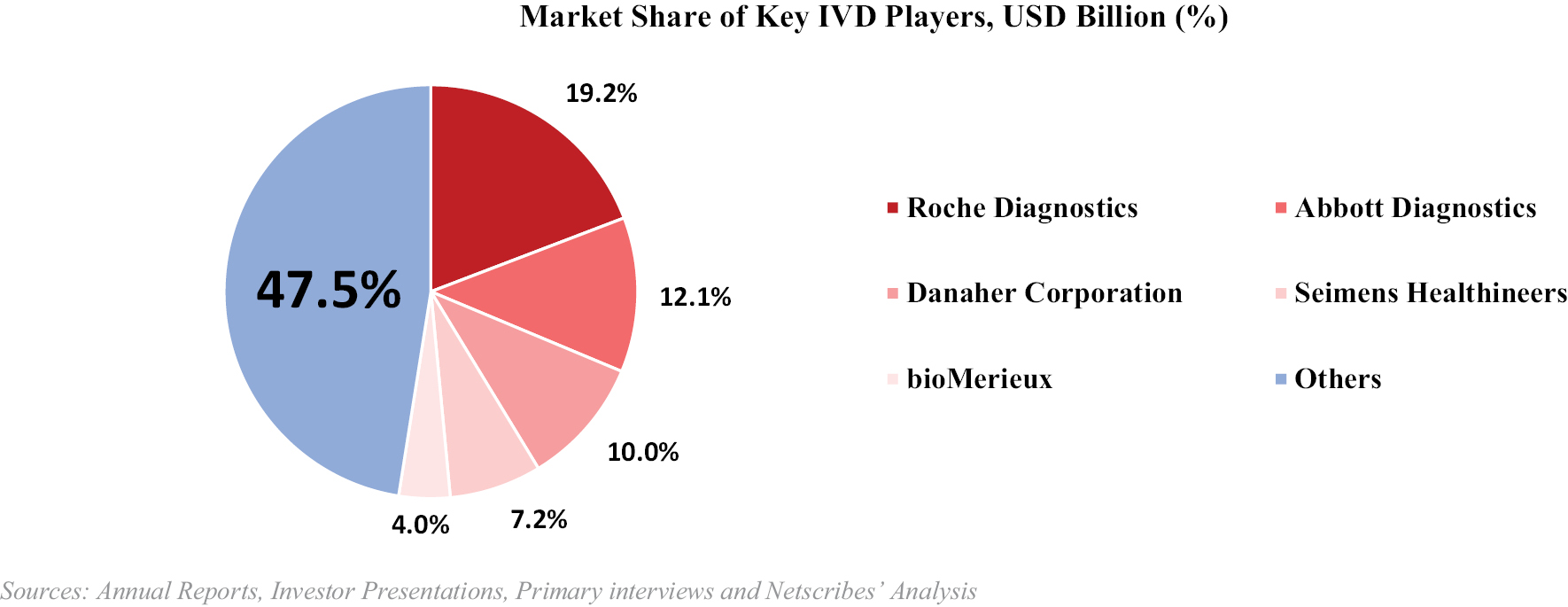

Our Industry

We compete in the in-vitro diagnostic (“IVD”) market. The IVD tests are defined as medical devices and reagents that are used to analyze specimens derived from the human body (including blood, tissues, and other body fluids) to detect diseases, conditions, and infections. IVD tests are usually performed at either stand-alone laboratory, hospital-based laboratory, or point-of-care (“POC”) centers. The technologies used for test sample preparation majorly include polymerase chain reaction (“PCR”), microarray techniques, sequencing technology, and mass spectrometry. Based on the key technologies involved, the global IVD market is fragmented into sub-segments including Immunoassay,

2

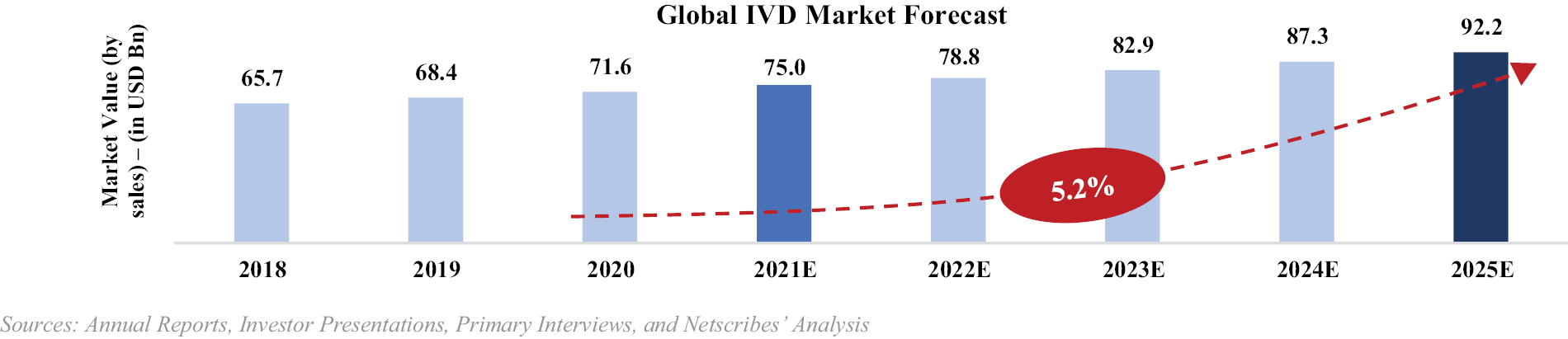

Hematology, Clinical Chemistry, Molecular Diagnostics, Microbiology, Haemostasias, Flow Cytometry and others. According to Netscribes’ estimates, the global IVD market was valued at around $75.0 billion (FY2021E). It has the potential to experience modest growth rates in the next five years, expanding at a CAGR of around 5.2% (2020 – 2025).

____________

Source: Annual Reports, Investor Presentations, Primary Interviews, and Netscribes’ Analysis

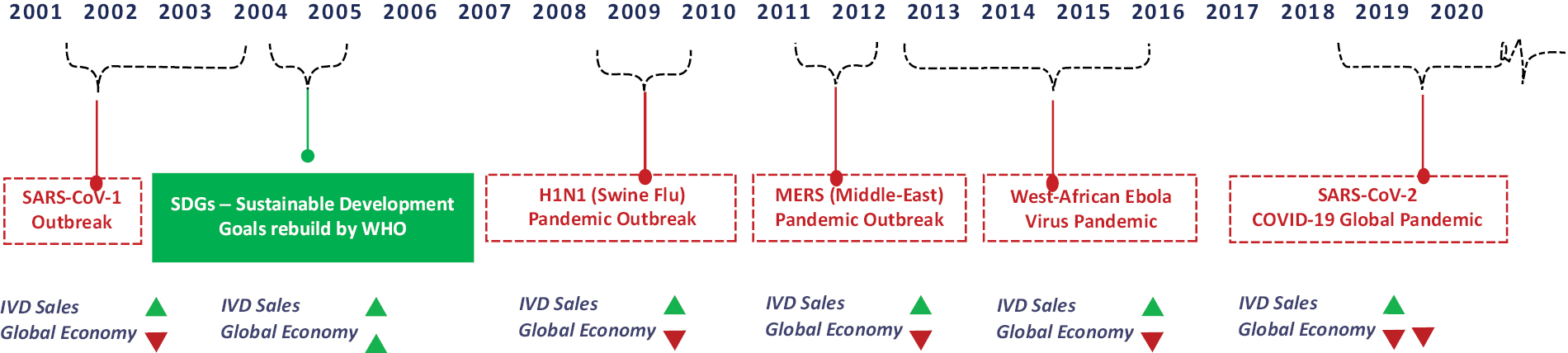

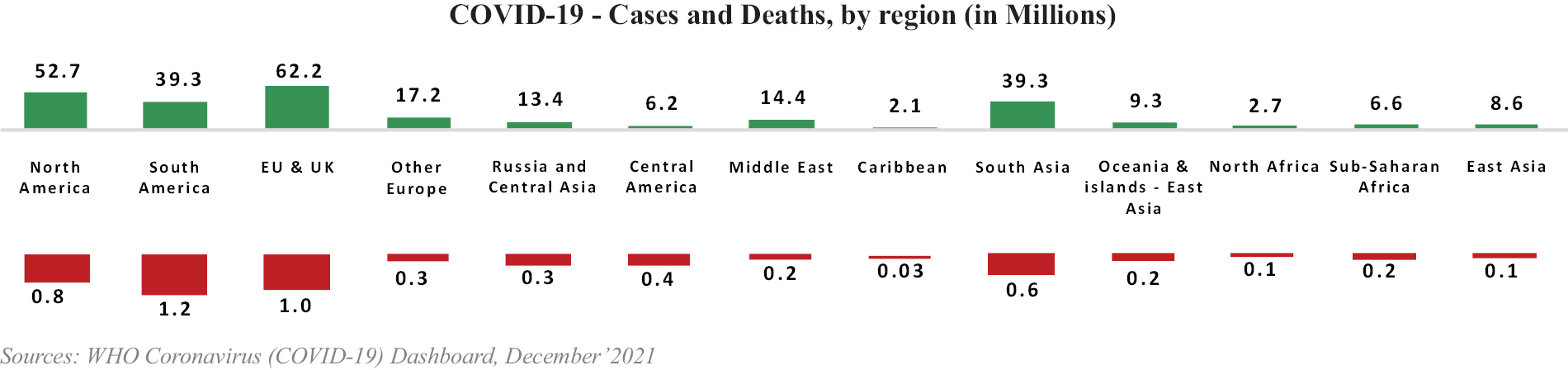

In light of the COVID-19 pandemic and healthcare being a non-satiable necessity to humankind, the IVD sector is ever-expanding and is expected to experience lucrative growth rates owing to driving factors such as aging global population, increase in the occurrence of complex infectious diseases, an increase in awareness among the global urban populations etc. However, lack of proper reimbursement policies in the developing nations and scepticism among patients to get regular healthcare consulting are still hindrances in some regions, especially third-world countries, which impedes the growth of the IVD market.

In recent years, the technological revolution that spans across industries, including healthcare, is a massive, inevitable and unparalleled one that the 21st century has seen. With digitalization being the torchbearer of this transformation, healthcare has been one of the most successful digitally-integrated industries. This is owing to its intensive capacity to absorb and adapt to new technology within traces of almost every domain existent. Technologies such as POC testing, liquid biopsy and molecular diagnostics have witnessed revolutionary advancements that are milestones to modern medicine.

Our Competitive Strengths

We believe the following competitive strengths differentiate us from our competitors and will continue to contribute to our success:

Cutting-edge technology. Our Group is a dynamic and innovative group engaged in creating cutting-edge technology. In particular, our in-development Virax Immune’s immunological diagnostic profiling technique is intended to be cutting-edge technology which is still not available on the IVD market as of the date of this prospectus, enabling our Group to radically change the diagnostic approaches of the IVD market with respect to major viral diseases.

Commercialization of our own diagnostic devices. Our Virax Immune suite of IVD T-Cell test kits, which are still currently being developed, are designed to be as lab agnostic and easy to use as possible. As a result, we believe this will allow us to distribute the T-Cell vitro diagnostics test kit to a broader geographic reach and deploy the test kits rapidly, without having to impose difficult techniques or equipment on our lab partners or being tied down to a specific lab partner. Further, although we entered into a non-binding letter of intent with a European Union based materials technology company to potentially partially acquire one of their proprietary technologies, the Virax Immune brand’s future success is not dependent on our ability to partially acquire this proprietary technology as we believe that the adoption of their proprietary technology into our immune system testing technology for use at point-of-care or outside of a laboratory will only further complement the functionalities of our upcoming Virax Immune IVD T-Cell test kit in the future. However, if we fail to partially acquire or fail to adapt the necessary proprietary technology, our competitors may manufacture and market similar products, or dilute our brands, which could adversely affect our potential market share under the Virax Immune brand or delay the introduction of our future products under Virax Immune brand to the market in the long term, and thus, it could have a material adverse effect on our planned business, financial condition and results of operations.

Advanced Technologies with Competitive Pricing. Our ViraxClear diagnostic test kits offer very high sensitivity and specificity levels, approximately 98 to 99% accuracy as compared to an industry average of approximately 90% accuracy, which allow consumers to obtain consistent test results with high accuracy. We established a procurement chain with various large Chinese and European biotechnology companies and manufacturers which enables us to offer our ViraxClear diagnostic test kits to consumers at competitive pricing.

3

Experienced Management Team with Extensive Industry Expertise and a Global Vision. Our Group has an experienced management team driven by a shared passion for the prevention, detection, diagnosis and risk management of viral diseases, in particular immunology. The team consists of members with diverse expertise whom possess keen insights into the latest trends in the global healthcare and pharmaceutical markets.

Robust Sales and Distribution Network. Our Group has built a strong sales and distribution network for our Virax branded products since 2020. Our sales and distribution network is composed of our own direct sales primarily through our e-commerce platform as well as various strategic distribution partners, located around the world. We have further complemented our sales and distribution network by securing distribution agreements for in-demand companies, brands and products to sell as an exclusive distributor on a regional basis. For example, under our ViraxClear brand, we have a third-party exclusive distribution agreement with PRC biotechnology company, Nanjing Vazyme Medical Technology Co., Ltd, for the distribution of their diagnostic kits under our brand name in the Canadian market. The third party exclusive distribution agreements allowed our Group to drive revenue and build further shareholders’ value by increase sales and sales margin on products that we do not produce.

Expanding Research and Development Capabilities. Our Group has invested significant resources with respect to our gross income in research and development. As of September 30, 2021, we have an intellectual property portfolio consisting of 16 regional exclusivity licenses, 3 pending trademarks and 4 registered domain names. We intend to apply for an aggregate of 3 patents in 2022. For one of the pending patents, we are in the process of acquiring it and we expect to close the acquisition in 2022. Further, we are developing a T-Cell IVD test kit under the Virax Immune brand for COVID-19 initially, which we subsequently intend to adapt for immunological profiling against multiple viral threats. We are also building a proprietary mobile application for Virax Immune, using an in-house code, that will present an individual’s immunological profiling data and provide advice on the users’ immune system. Based on our management team’s analysis, we expect to file a patent for the Virax Immune Cell diagnostic test kit and a copyright for the Virax Immune app in 2022. For further details, please refer to “Business — Intellectual Property” section. As of September 30, 2021, our research and development team was composed of 4 personnel, which accounted for approximately 33.3% of our total employees. While Mr. James Foster and Mr. Cameron Shaw fulfiled their duties as chief executive officer and chief operating officer, respectively, they were also included in the research and development team in addition to Mr. Mark Ternouth, our Chief Technical Officer, and Mr. Tomasz George, our Chief Scientific Officer, due to their respective inputs and assistance to the innovations and developments of the ViraxClear, ViraxCare and Virax Immune business lines. Our research and development team has years of technology know-how in developing and launching products and services in response to market demands.

Our Strategies

Our goal is to become one of the leading global biotechnology pioneers in the field of IVD testing and immunology. We aim to achieve this goal by implementing the following strategies:

• Development of the proprietary Virax Immune suite of IVD T-Cell test kits, which has a huge potential in immunology diagnostics and therapeutics, and development of the Virax Immune Mobile Application that will allow consumers to access their test results and then link to a variety of information and advice regarding their immunological profile provided by their test results.

• Expand Sales and Marketing.

• Further collaborating with international industry leaders as well as governments by selectively pursuing strategic partnerships, investments, or acquisitions.

• Penetrating other mature regions or countries through the provision of our disruptive technology.

• Expand our sales team.

• Strategic acquisitions of biotechnology companies with the intention of turning Virax into a fully integrated vehicle.

4

Our Challenges

We face risks and uncertainties in realizing our business objectives and executing our strategies, including but not limited to, those relating to:

• Our ability to successfully obtain regulatory approvals for our Virax Immune products, namely, T-Cell IVD Test. Any failure to obtain regulatory approval would adversely affect our ability to commercialize our Virax Immune products in the expected timeframe or at all, and our ability to expand our business and achieve our strategic objectives would be impaired.

• Our ability to navigate the dynamic regulatory environment for IVD. Any change in the procedure for obtaining approvals for various global marketplaces might adversely affect Virax’s ability to enter various markets for any new product candidates and the sales of our products in new markets.

• Our ability to successfully leverage on the Virax Immune platform to discover, develop and commercialize additional products and services;

• Our ability to develop T-Cell IVD Test under the Virax Immune brand successfully, and yield the insights that we expect or on a timetable that allows us to develop or commercialize any new diagnostic products;

• Our ability to proceed through clinical and validation studies successfully of our proprietary technology T-Cell testing under the Virax Immune brand; and

• Our ability to discover and continuously develop products and services related to major viral threats and COVID-19 under the Virax Immune brand.

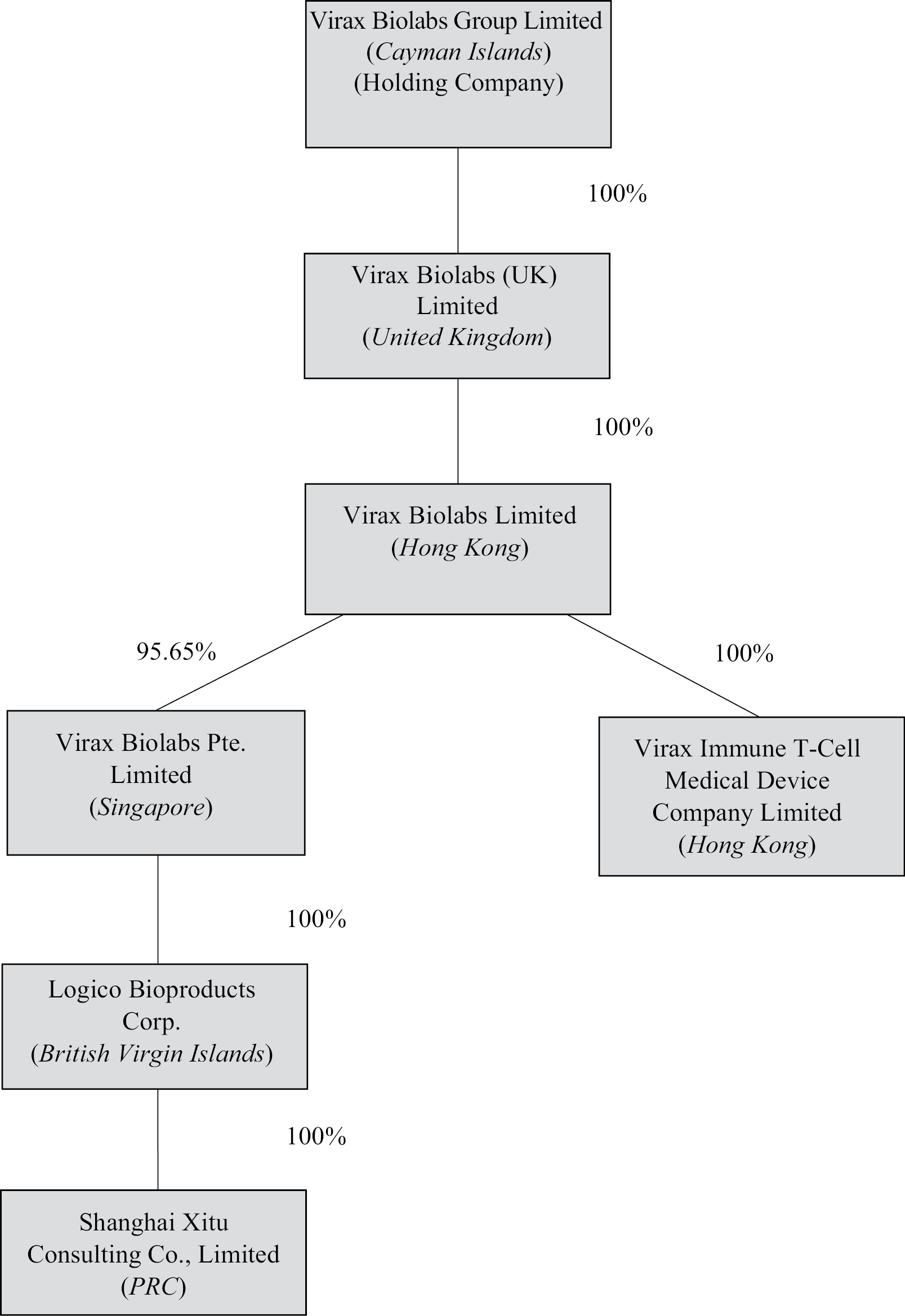

Corporate History and Structure

Structural Overview

Virax Cayman is a holding company incorporated in the Cayman Islands that owns all of the outstanding capital stock of Virax Biolabs (UK) Limited, our wholly-owned United Kingdom subsidiary. Virax Biolabs (UK) Limited, in turn, owns all of the outstanding capital stock of Virax Biolabs Limited, our wholly-owned Hong Kong subsidiary. Virax Biolabs Limited owns all of the outstanding capital stock of Virax Immune T-Cell Medical Device Company Limited, our wholly-owned Hong Kong subsidiary, and 95.65% of the outstanding capital stock of Virax Biolabs Pte. Limited, our operating subsidiary incorporated in Singapore. Virax Biolabs Pte. Limited owns all of the outstanding capital stock of Logico Bioproducts Corp., a wholly-owned British Virgin Islands and a subsidiary of Virax Biolabs Pte. Limited. Logico Bioproducts Corp., in turn, owns all of the outstanding capital stock of Shanghai Xitu, a wholly-owned subsidiary of Logico Bioproducts Corp. and a wholly foreign owned enterprise based in China.

We completed a reorganization and share exchange of our company in September 2021 (the “Reorganization”). Pursuant to the Reorganization, all shareholders of Virax Biolabs Limited (HK) transferred their shares, 102,478,548 ordinary shares in total, to Virax Biolabs (UK) Limited, in exchange for an aggregate of (i) 2,549,028 newly issued Class A Ordinary Shares and (ii) 7,034,306 newly issued Class B Ordinary Shares of Virax Biolabs Group Limited. On June 19, 2022, Virax Cayman underwent a shareholding restructuring whereby the Company’s authorized share capital became a single class of shares of Ordinary Shares and all of the then issued shares were re-designated as Ordinary Shares.

Organization Structure and Purpose

Virax Biolabs Group Limited (“Virax Cayman”) — Virax Biolabs Group Limited is a Cayman Islands exempted company incorporated on September 2, 2021, previously named as “Virax Biolabs (Cayman) Limited” and effected a name change to “Virax Biolabs Group Limited” on January 19, 2022. Structured as a holding company with no material operations, Virax Cayman conducts our operations through its operating subsidiaries in the Hong Kong, Singapore, British Virgin Islands and China.

5

Virax Biolabs (UK) Limited — Virax Biolabs (UK) Limited was incorporated on August 19, 2021 under the laws of the United Kingdom, a wholly-owned subsidiary of Virax Cayman and structured as a holding company with no material operations.

Virax Biolabs Limited (“HKco”) — Virax Biolabs Limited, incorporated on April 14, 2020 under the laws of Hong Kong, was previously named as “Shanghai Biotechnology Devices Limited” and effected a name change to “Virax Biolabs Limited” on July 12, 2021. Virax Biolabs Limited, our wholly-owned Hong Kong subsidiary, serves as a holding company.

Virax Immune T-Cell Medical Device Company Limited (“Virax Immune T-Cell”) — Virax Immune T-Cell Medical Device Company Limited, a wholly-owned subsidiary of HKco, incorporated on January 16, 2017 under the laws of Hong Kong, was previously named as “Stork Nutrition Asia Limited” and effected a name change to “Virax Immune T-Cell Medical Device Company Limited” on September 10, 2021. It is primarily engaged in the research and development of T-Cell blood analysis.

Virax Biolabs Pte. Limited (“SingaporeCo”) — Virax Biolabs Pte. Limited, incorporated on May 4, 2013 under the laws of Singapore, was previously named as “Natural Source Group Pte. Limited” and effected a name change to “Virax Biolabs Pte. Limited” on July 2, 2021. 95.65% of its capital stock is owned by Virax Biolabs Limited and the remaining 4.35% is owned by independent third party shareholders. It is our operating company, primarily engaged in the trading and sales of our products and running primarily day to day operations.

Logico Bioproducts Corp. (“Logico BVI”) — Logico Bioproducts Corp., a wholly-owned subsidiary of SingaporeCo, is a limited liability company incorporated in the British Virgin Islands on January 21, 2011, and is primarily engaged in the trading and sales of our products.

Shanghai Xitu Consulting Co., Limited (“Shanghai Xitu”) — Shanghai Xitu, a wholly-owned subsidiary of Logico BVI and a wholly foreign owned enterprise, is a limited liability company incorporated on October 27, 2017 in China. Shanghai Xitu is primarily engaged in procurement.

6

The following diagram illustrates our corporate structure immediately following the consummation of this offering:

Government Regulations and Approvals for this Offering

As some of our operations are currently conducted through our operating entities established in Hong Kong and Shanghai, namely, HKco, Virax Immune T-Cell, Shanghai Xitu, we are potentially subject to significant regulations by various agencies of the Chinese government. The Regulations on Mergers and Acquisitions of Domestic Companies by Foreign Investors, or the M&A Rules, adopted by six PRC regulatory agencies in 2006 and amended in 2009, require

7

an overseas special purpose vehicle formed for listing purposes through acquisitions of PRC domestic companies and controlled by PRC companies or individuals to obtain the approval of the CSRC and Ministry of Commerce of the PRC (“MOFCOM”), prior to the listing and trading of such special purpose vehicle’s securities on an overseas stock exchange. Substantial uncertainty remains regarding the scope and applicability of the M&A Rules to offshore special purpose vehicles. As at the date of this prospectus, we have been advised by Zhong Lun Law Firm that CSRC’s approval under the M&A Rules is not required for the listing and trading of our Ordinary Shares on Nasdaq in the context of this offering given that we are an exempted company with limited liability incorporated under the laws of the Cayman Islands with some operations located in Hong Kong and the PRC controlled by non-PRC citizens. As such, we do not fit into the definition of “overseas special purpose vehicle” under the M&A Regulations and we have never conducted any merger or acquisitions of any PRC domestic companies with a related party relationship. MOFCOM’s approval under the M&A Rules is also not required as we have never conducted any merger or acquisitions of any PRC domestic companies with a related party relationship. We cannot assure you that relevant PRC governmental agencies, including the CSRC, would reach the same conclusion as we do. If we or our subsidiaries inadvertently conclude that such approval is not required, our ability to offer or continue to offer our Ordinary Shares to investors could be significantly limited or completed hindered, which could cause the value of our Ordinary Shares to significantly decline or become worthless. Our Group or Shanghai Xitu may also face sanctions by the CSRC, the CAC or other PRC regulatory agencies. These regulatory agencies may impose fines and penalties on our operations in China, limit our ability to pay dividends outside of China, limit our operations in China, delay or restrict the repatriation of the proceeds from this offering into China or take other actions that could have a material adverse effect on our business, financial condition, results of operations and prospects, as well as the trading price of our securities.

On July 6, 2021, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the Opinions on Strictly Cracking Down on Illegal Securities Activities According to Law (the “Opinions”), which called for strengthened regulation over illegal securities activities and supervision on overseas listings by China-based companies and propose to take effective measures.

As at the date of this prospectus, no official guidance or related implementation rules have been issued in relation to the Opinions, and the interpretation and implementation of the Opinions also remain unclear to some extent at this stage. Based on our understanding of the current PRC laws and regulations in effect at the time of this prospectus, no prior permission is required under the M&A Rules or the Opinions from any PRC governmental authorities (including the CSRC) for consummating this offering by our company as advised by our PRC legal adviser, Zhong Lun Law Firm. However, there can be no assurance that the relevant PRC governmental authorities, including the CSRC, would reach the same conclusion as us, or that the CSRC or any other PRC governmental authorities would not promulgate new rules or new interpretation of current rules (with retrospective effect) to require us to obtain CSRC or other PRC governmental approvals for this offering. If we or our subsidiaries inadvertently conclude that such permission is not required, our ability to offer or continue to offer our Ordinary Shares to investors could be significantly limited or completed hindered, which could cause the value of our Ordinary Shares to significantly decline or become worthless. Our Group or Shanghai Xitu may also face sanctions by the CSRC, the CAC or other PRC regulatory agencies. These regulatory agencies may impose fines and penalties on our operations in China, limit our ability to pay dividends outside of China, limit our operations in China, delay or restrict the repatriation of the proceeds from this offering into China or take other actions that could have a material adverse effect on our business, financial condition, results of operations and prospects, as well as the trading price of our securities.

On December 28, 2021, the Cyberspace Administration of China (the “CAC”), published the Measures for Cybersecurity Review which became effective on February 15, 2022, which required that any “network platform operator” controlling personal information of no less than one million users which seeks to list on a foreign stock exchange should also be subject to cybersecurity review. The PRC Data Security Law, which took effect on September 1, 2021, imposes data security and privacy obligations on entities and individuals that carry out data activities, provides for a national security review procedure for data activities that may affect national security and imposes export restrictions on certain data and information. On August 20, 2021, the Standing Committee of the People’s Congress promulgated the PRC Personal Information Protection Law (the “PIPL”), which took effect on November 1, 2021. The PIPL sets out the regulatory framework for handling and protection of personal information and transmission of personal information to overseas. Shanghai Xitu is not a network platform operator, nor do we conduct data activities that may affect national security or hold personal information of more than one million users. In addition, we do not conduct any cross border transfer of personal information from the PRC to other jurisdictions. As such, we do not believe the Virax Group falls in the “operators of critical information infrastructure” as mentioned above and we are

8

not subject to PRC cybersecurity review. However, the Measures for Cybersecurity Review (2021 version), the Data Security Law and the PIPL were recently adopted and remain unclear on how they will be interpreted, amended and implemented by the relevant PRC governmental authorities.

On December 24, 2021, the State Council published the draft Administrative Provisions on the Overseas Issuance and Listing of Securities by Domestic Companies (Draft for Comments) (the “Administrative Provisions”), and the CSRC published the draft Measures for Record-filings of the Overseas Issuance and Listing of Securities by Domestic Companies (Draft for Comments) (the “Administrative Measures”), for public comment. It should be noted that neither the Administrative Provisions nor the Administrative Measures have come into effect as of the date of this registration statement.

Pursuant to the Article 2 of the Administrative Measures, domestic enterprises that directly or indirectly offer or list securities on an overseas stock exchange shall file with the CSRC. We are not “directly” offering securities overseas (as Shanghai Xitu is not the issuer of the listed securities on an overseas stock exchange). According to the Administrative Measures, if the issuer meets the following conditions, it shall be deemed as an “indirect” overseas offering and listing of a domestic enterprise:

(1) the operating income, total profit, total assets or net assets of the domestic enterprise in the most recent fiscal year account for more than 50% of the relevant data in the issuer’s audited consolidated financial statements for the same period;

(2) most of the senior management personnel responsible for business operation and management are Chinese Citizens or having a ordinary residence located in the PRC, and the principal place of business operation is located in or mainly within the PRC.

Based on the above mentioned Administrative Provisions and Administrative Measures (both are in draft form only), as advised by our PRC legal adviser, Zhong Lun Law Firm, given that the operating income, total profit, total assets or net assets of the Shanghai Xitu for the last financial year accounted for less than 50% of the Virax Group’s audited consolidated financial statements and none of Shanghai Xitu’s senior management personnel is a PRC Citizen and only two (2) out of seven (7) have an ordinary residence located in the PRC, this offering shall not be deemed as a domestic enterprise that indirectly offer or list securities on an overseas stock exchange, nor does it requires filing or approvals from the CSRC. However, there can be no assurance that the relevant PRC governmental authorities, including the CSRC, would reach the same conclusion as us, or that the CSRC or any other PRC governmental authorities would not promulgate new rules or new interpretation of current rules (with retrospective effect) to require us to obtain CSRC or other PRC governmental approvals for this offering. If we or our subsidiaries inadvertently conclude that such approvals are not required, our ability to offer or continue to offer our Ordinary Shares to investors could be significantly limited or completed hindered, which could cause the value of our Ordinary Shares to significantly decline or become worthless. Our Group or Shanghai Xitu may also face sanctions by the CSRC, the CAC or other PRC regulatory agencies. These regulatory agencies may impose fines and penalties on our operations in China, limit our ability to pay dividends outside of China, limit our operations in China, delay or restrict the repatriation of the proceeds from this offering into China or take other actions that could have a material adverse effect on our business, financial condition, results of operations and prospects, as well as the trading price of our securities.

We have been closely monitoring regulatory developments in China regarding any necessary approvals from the CSRC or other PRC governmental authorities required for overseas listings, including this offering. Our business may be subject to various government regulations and regulatory interference. As of the date of this prospectus, we have been advised by Zhong Lun Law Firm, our PRC legal adviser, that (i) Shanghai Xitu has obtained all necessary permissions or approvals and authorizations in the PRC in all material aspects in relation to conducting its business operations in China; and (ii) we are not required to obtain any permission or approval from any PRC authority to issue securities to foreign investors (by Virax Cayman) or in connection with this offering under PRC laws or regulations in effect. Except for the business license issued by the local branch of the State Administration for Market Regulation, which Shanghai Xitu’s have obtained and are in full force and effect as of the date of this prospectus, Shanghai Xitu is not required to obtain any other licenses, approvals or permits to conduct its business operations in China. To the best of our knowledge, as of the date of this prospectus, there are no laws or regulations that are or will be adopted in the near future by PRC government authorities that would prevent Shanghai Xitu from maintaining the business license it has obtained or would require it to obtain additional licenses or qualifications in order to operate its current business operations. Further, there are no PRC laws and regulations (including the CSRC, the CAC, or any other

9

government entity) in force explicitly requiring that our Group or Shanghai Xitu to obtain permission from PRC authorities for this offering or to issue securities to foreign investors (by Virax Cayman) and we are not required to obtain additional permission or approval from Chinese authorities, including the CSRC and the CAC, to either approve our PRC subsidiaries’ operation or to offer the securities (of Virax Cayman) being registered to foreign investors. Nevertheless, we may incur increased costs necessary to comply with existing and newly adopted laws and regulations or penalties for any failure to comply. Furthermore, given recent statements by the Chinese government indicating an intent to exert more oversight and control over offerings that are conducted overseas, although as of the date of this prospectus, our Group or Shanghai Xitu have not been involved in any investigations initiated by the applicable governmental regulatory authorities, nor have we received any inquiry, notice, warning, or sanction in such respect, there remains uncertainty as to the enactment, interpretation and implementation of regulatory requirements related to overseas securities offerings and other capital markets activities. If it is determined in the future that the approval of the CSRC, the CAC or any other regulatory authority is required for this offering, our Group or Shanghai Xitu may face sanctions by the CSRC, the CAC or other PRC regulatory agencies. These regulatory agencies may impose fines and penalties on our operations in China, limit our ability to pay dividends outside of China, limit our operations in China, delay or restrict the repatriation of the proceeds from this offering into China or take other actions that could have a material adverse effect on our business, financial condition, results of operations and prospects, as well as the trading price of our securities. The CSRC, the CAC or other PRC regulatory agencies also may take actions requiring us, or making it advisable for us, to halt this offering before settlement and delivery of the Ordinary Shares that we are offering. Consequently, if you engage in market trading or other activities in anticipation of and prior to settlement and delivery of the Ordinary Shares that we are offering, you do so at the risk that settlement and delivery may not occur. In addition, if the CSRC, the CAC or other regulatory PRC agencies later promulgate new rules requiring that our Group or Shanghai Xitu obtain their approvals for this offering, our Group or Shanghai Xitu may be unable to obtain a waiver of such approval requirements, if and when procedures are established to obtain such a waiver. Any uncertainties and/or negative publicity regarding such an approval requirement could have a material adverse effect on our ability to complete this offering or any follow-on offering of our securities or the market for and market price of our ordinary shares, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless. See “Risk Factors — Risks Related to Doing Business in China and Hong Kong — The approval of the China Securities Regulatory Commission and other PRC governmental authorities are not required in connection with this offering, and, if required, we cannot predict whether we will be able to obtain such approval,” “Risk Factors — Risks Related to Doing Business in China and Hong Kong — The Chinese government exerts substantial influence over the manner in which we must conduct our business activities, and, may intervene or influence our operations at any time, or may exert more oversight and control over offerings conducted overseas, which could significantly limit or completely hinder our ability to offer or continue to offer our Ordinary Shares to investors and could cause the value of our Ordinary Shares to significantly decline or become worthless.”

Transfer of Cash Through our Organization

Currently, Virax Cayman is incorporated in Cayman Islands to be the ultimate parent company of the Group. As a holding company with no material operations of our own, Virax Cayman conduct our operations through our operating subsidiaries established in Singapore, Hong Kong, China, and the British Virgin Islands. Currently, Virax Cayman indirectly owns 95.65% of the equity interests in SingaporeCo. However, some of our operations are currently conducted through our operating entities established in Hong Kong and Shanghai, primarily, Virax Immune T-Cell Medical Device Company Limited and Shanghai Xitu Consulting Co., Limited, which we refer to as Virax Immune T-Cell and Shanghai Xitu, respectively. Virax Cayman is permitted under the laws of Cayman Islands to provide funding to our subsidiaries in Singapore, British Virgin Islands, Hong Kong and Shanghai through loans or capital contributions on the amount of the funds. Virax Cayman can distribute earnings from its businesses, including subsidiaries, to the U.S. investors as well as the ability to settle amounts owed under intercompany agreements. Our operations in Singapore, British Virgin Islands, Hong Kong and Shanghai were in loss position since 2020, and the Group has raised capital through financing transactions and provided funding to our operations.

Our operating subsidiaries are permitted under the laws of Singapore, British Virgin Islands, PRC and Hong Kong, respectively, to provide funding to Virax Cayman, the holding company incorporated in the Cayman Islands through dividend distributions. Our Group currently intend to retain all available funds and future earnings, if any, for the operation and expansion of our business and do not anticipate declaring or paying any dividends in the foreseeable future. We currently do not have any dividend policy, and we do not anticipate declaring or paying dividends in

10

the foreseeable future. We intend to retain all available funds and any future earnings to fund the development and expansion of our business. If our subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict their ability to pay dividends to us. As of the date of this prospectus, there were no cash flows between our subsidiaries, and no cash flows between our Virax Cayman and our subsidiaries.

Currently, some of our operations are currently conducted through our operating entities established in Hong Kong and Shanghai. We did not have or intend to set up any subsidiary or enter into any contractual arrangements to establish a VIE structure with any entity in China. Since Hong Kong is a special administrative region of the PRC and the basic policies of the PRC regarding Hong Kong are reflected in the Basic Law, providing Hong Kong with a high degree of autonomy and executive, legislative and independent judicial powers, including that of final adjudication under the principle of “one country, two systems”. Under Hong Kong law, dividends could only be paid out of distributable profits (that is, accumulated realized profits less accumulated realized losses) or other distributable reserves. Dividends cannot be paid out of share capital. Under the current practice of the Inland Revenue Department of Hong Kong, no tax is payable in Hong Kong in respect of dividends paid by us.

Further, the PRC government imposes controls on the convertibility of RMB into foreign currencies and, in certain cases, the remittance of currency out of China. The dividends and distributions from Shanghai Xitu is subject to relevant regulations and restrictions on dividends and payment to parties outside of China. See “Risk Factors — Risks Related to Doing Business in China and Hong Kong — PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay us from using part of the proceeds of this offering to make loans or additional capital contributions to our PRC subsidiary, which could materially and adversely affect our liquidity and our ability to fund and expand our business” and “Restrictions on currency exchange may limit our ability to utilize our revenues effectively” for more information on the risk of PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion with respect to part of the proceeds of this offering to make loans or additional capital contributions to our PRC subsidiary and restrictions on currency exchange may limit our ability to utilize our revenues effectively with respect to our operations. Further, investment in Chinese companies, which are governed by the Foreign Investment Law and Company Law, and the dividends and distributions from Shanghai Xitu is subject to relevant regulations and restrictions on dividends and payment to parties outside of China. Applicable PRC law permits payment of dividends to Virax Cayman by Shanghai Xitu only out of its net income, if any, determined in accordance with PRC accounting standards and regulations. Shanghai Xitu is required to set aside a portion of its net income, if any, each year to fund general reserves for appropriations until such reserves have reached 50% of the relevant entity’s registered capital. These reserves are not distributable as cash dividends. A PRC company is not permitted to distribute any profits until any losses from prior fiscal years have been offset. Profits retained from prior fiscal years may be distributed together with distributable profits from the current fiscal year. In addition, registered share capital and capital reserve accounts are also restricted from withdrawal in the PRC, up to the amount of net assets held in each operating subsidiary.

Within the organization, investor cash inflows have all been received by Virax Cayman. Cash to fund Virax Cayman’s operations is transferred from Virax Cayman down through our Singapore, Hong Kong, BVI entities and then into our Chinese entity through capital contributions and loans. Transfers among our Singapore and Hong Kong entities are not restricted. Furthermore, subject to payment of withholding taxes, there are no restrictions and limitations on our ability to distribute earnings from our subsidiaries to Virax Cayman and U.S. investors as well as the ability to settle amounts owed under any agreements. No dividends or distribution have been made by our subsidiaries or by Virax Cayman to date and we intend to reinvest all cash into our subsidiaries for the foreseeable future. For the years ended March 31, 2021 and 2020 and for the six months ended September 30, 2021, there was no transfer of funds between Virax Cayman and its subsidiaries.

Further, subject to the Companies Act and our Second Amended and Restated Memorandum and Articles of Association, our board of directors may authorize and declare a dividend to shareholders from time to time out of the profits from Virax Cayman, realized or unrealized, or out of the share premium account, provided that Virax Cayman will remain solvent, meaning Virax Cayman is able to pay its debts as they come due in the ordinary course of business. There is no further Cayman Islands statutory restriction on the amount of funds which may be distributed by us in the form of dividends.

There are no restrictions or limitations under the laws of Singapore imposed on the conversion of Singapore dollars into foreign currencies and the remittance of currencies out of Singapore, nor is there any restriction on any foreign exchange to transfer cash between Virax Cayman and its subsidiaries, across borders and to foreign investors

11

outside of Singapore, nor is there any restrictions and limitations to distribute earnings from the subsidiaries, to Virax Cayman and investors outside of Singapore and amounts owed as well as the ability to settle amounts owed under intercompany agreements. There are no foreign exchange controls in Singapore. For the years ended March 31, 2021 and 2020 and for the six months ended September 30, 2021, there was no transfer between Virax Cayman and its subsidiaries. As of the date of this prospectus and for the year ended March 31, 2021 and 2020, we have not declared any dividend. If we determine to pay dividends on any of our Ordinary Shares in the future, as a holding company, we will be dependent on receipt of funds from our operating subsidiaries in Singapore, British Virgin Islands and Hong Kong. Under the current practice of the Inland Revenue Authority of Singapore, no tax is payable in Singapore, in respect of dividends paid by us, and under the current laws of the Cayman Islands, we are also not subject to tax on income or capital gains and withholding tax is not imposed upon payments of dividends from Virax Cayman to its shareholders. Under the current practice of the Inland Revenue Department of Hong Kong, no tax is payable in Hong Kong in respect of dividends paid by us. Further, we do not have specific cash management policies and procedures in place that dictate how funds are transferred through our organization, however, we have been closely monitoring our transfer of funds and will adopt relevant policies and procedures if necessary.

See “Risk Factors — Risk Related to Our Corporate Structure — We may rely on dividends and other distributions on equity paid by our subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our subsidiaries to make payments to us could have a material adverse effect on our ability to conduct our business.” for more information.

Risk Factor Summary

Our business and our offering are subject to a number of risks, including risks that may prevent us from achieving our business objectives or may materially and adversely affect our business, financial condition, results of operations, cash flows and prospects that you should consider before making a decision to invest in our Ordinary Shares. These risks are discussed more fully in “Risk Factors” beginning on page 21. These risks include, but are not limited to, the following:

• We have limited operating history, have incurred operating losses for the six months ended September 30, 2021 and the years ended March 31, 2021 and 2020 and expect to incur significant losses for the foreseeable future. We may not generate sufficient revenue or become profitable or, if we achieve profitability, we may not be able to sustain it. Therefore, it is too early to draw meaningful conclusions from the financial performance of the Group due to the change in our business focus since 2020 as our commercialized brands are ViraxClear and ViraxCare, which have been put into market since 2020. Further, our ViraxClear brand is a diagnostics distributor that primarily distributes COVID-19 IVD tests kits that we source from third parties.

• We expect to make significant investments with respect to our gross income in our continued research and development of new products and services, which may not be successful.

• Our efforts to develop T-Cell In-Vitro Diagnostic Test may not be successful, and it may not yield the insights we expect at all or on a timetable that allows us to develop or commercialize any new diagnostic products.

• If we are not successful in obtaining regulatory approvals for our Virax Immune products, we may not be able to commercialize our products in the expected timeframe or at all, and our ability to expand our business and achieve our strategic objectives would be impaired.

• We will face significant challenges in successfully commercializing our products.

• Our business, financial condition and results of operations will depend on the market acceptance and increased demand of our products by hospitals, governments and public health departments, as well as physicians others in the medical community, and the growing proportion of the population who are interested in taking personal charge over their health and wellbeing.

• The success of some of our products significantly depends on the continued demand for diagnostic and products linked to COVID-19 and other major viral diseases.

• The success of our proprietary technology T-Cell testing requires us to proceed through clinical and validation studies successfully, which is not guaranteed.

12

• The regulatory environment for IVD could change, resulting a new procedure for achieving approvals for various global marketplaces which might adversely affect Virax’s ability to enter various markets.

• During the development and validation of the T-Cell test there may be unforeseen biological or laboratory based variations in the samples or processes that could affect the course of test development and subsequent sensitivity and specificity of the test.

• The reliability of T-Cell test may not be exactly replicated in a clinical use environment as compared to our laboratory test conditions.

• The occurrence of supply chain, or sourcing issues for test components may disrupt the test development process causing delays.

• There is no guarantee that the sensitivity and specificity of T-Cell test will be sufficient.

• The specific subject groups needed for the clinical validation study may prove to be insufficient, too hard to identify or recruit, or subject numbers may be too large to easily recruit and conduct a trial.

• Registration of intellectual property rights for the T-Cell test procedure may prove to be impossible.

• Notified bodies such as the FDA or MHRA may make unrealistic requests of us and our test before it is accepted for use.

• The proposed intended use of the test may not be feasible, or the demand for this test in the market may decrease.

• The continuity, consistency and/or production capacity of test components and reagents may change over time, affecting test quality.